EPOS

What Is A2A Payment? Meaning, How It Works and Benefits

Thu, 12 Mar 2026 09:56:09 GMT

Speak to our Hyperlocal Expert

A2A payment or account-to-account payment moves money directly from one bank account to another, bypassing card networks and payment processors entirely. These real-time transfers offer lower costs, reduced fraud risk, and improved cash flow for businesses globally.

No intermediaries. No MDR. No settlement lag. The technology has existed for years. What changed is accessibility. Open banking regulations opened the infrastructure. Real-time rails made transfers instant. Digital onboarding made it practical for businesses of every size.

According to McKinsey, A2A payments now represent over 25% of global digital payment volumes. In India, Brazil, and across Europe, account to account payment rails have become the primary infrastructure for moving money between businesses and consumers.

This guide covers what A2A payment means, how it works, the different types, real-world applications, advantages and disadvantages, and how distribution-heavy businesses are embedding A2A inside their operations.

What Is an A2A Payment?

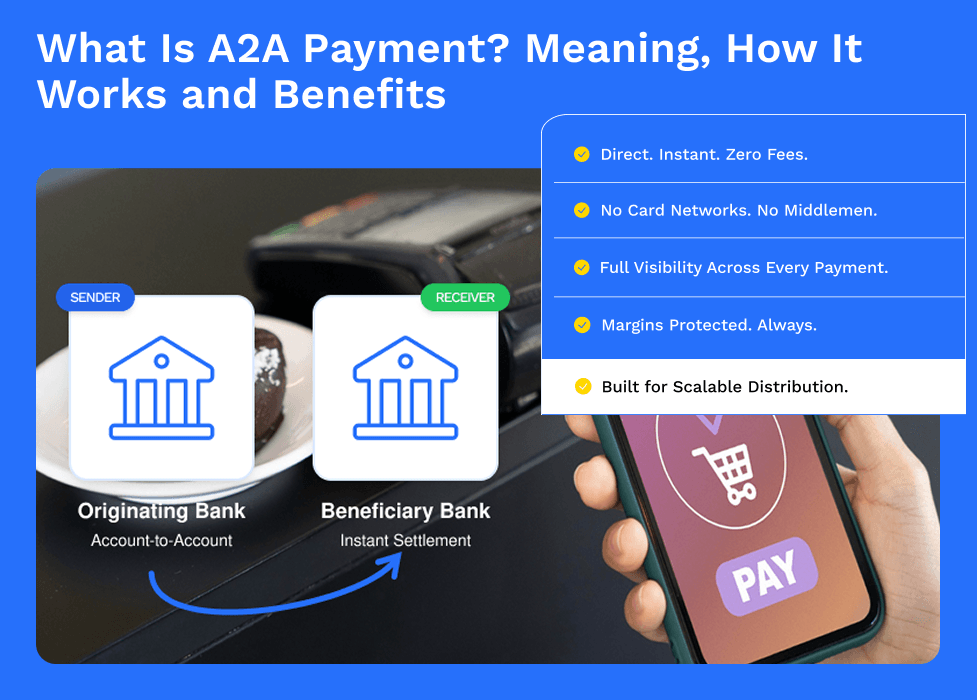

Account-to-account (A2A) payment transfers funds directly between two bank accounts without card networks, payment processors, or intermediaries. The payer's account is debited. The payee's account is credited. Nothing in between.

A2A stands for Account-to-Account. It describes any transaction where money moves directly from one bank account to another, whether between two individuals, two businesses, or a business and a consumer.

A simple example. A business pays a distributor directly from its corporate bank account. No card. No payment gateway taking a percentage. The distributor's account is credited instantly. That's an A2A payment. Same principle when a consumer pays for an online order directly from their bank account instead of entering card details. Direct, instant, traceable.

A2A vs P2P: What Is the Difference?

P2P payments are a subset of A2A. All P2P payments are A2A but not all A2A payments are P2P.

A2A | P2P | |

| Who uses it | Individuals and businesses | Individuals only |

| Transaction type | B2B, B2C, C2B, P2P | Person to person only |

| Examples | Payroll, supplier payments, refunds | Splitting bills, sending money to friends |

| Infrastructure | Bank rails, open banking APIs | Mobile apps, digital wallets |

A2A vs Pay by Bank: What Is the Difference?

Pay by Bank is a consumer-facing product built on A2A infrastructure. When a customer clicks "Pay by Bank" at checkout they're completing an A2A payment initiated through open banking APIs.

A2A is the underlying infrastructure. Pay by Bank is one application built on top of it.

Types of A2A Payments

There are several types of account to account payments, each meeting the needs of different transactional relationships and scenarios.

1. Push Payments

The payer initiates the transfer directly. They provide the recipient's bank details, authorise the payment, and the money moves. Ideal for one-off transactions, supplier invoice payments, and instant bank transfers where the payer controls timing and amount.

2. Pull Payments

The recipient initiates the transaction with the payer's prior authorisation. Commonly used for subscriptions, direct debits, and recurring bill payments. The payer authorises once through a direct debit mandate or payment initiation service. Payments happen automatically after that.

3. Open Banking and API Payments

These utilise APIs to enable secure, fast, and cost-effective direct bank transfers. Third-party providers access bank account data through open banking frameworks to initiate A2A payments without card networks. Often used as a direct alternative to card payments in e-commerce and business transactions.

4. Real-Time A2A Payments

Instant, 24/7 account-to-account transfers that settle in seconds. No batch processing. No overnight clearing windows. Networks like UPI in India, Faster Payments in the UK, PIX in Brazil, and SEPA Instant in Europe all operate on real-time A2A rails.

5. Scheduled A2A Payments

Set to trigger at a specific date and time. Payroll runs, supplier settlement cycles, and recurring vendor payments. Scheduled account-to-account payments give businesses predictability and control over cash flow without manual intervention each time a payment is due.

Common A2A Payment Use Cases by Relationship Type

Type | Description | Example |

B2B | Between businesses for goods, services, or operational costs | Supplier invoice payments |

B2C | Business to consumer for refunds, rebates, or payroll | Salary payments, instant refunds |

C2B | Consumer pays business directly from bank account | Online shopping, bill payments |

P2P | Individual to individual via mobile apps or platforms | Splitting bills, sending money to friends |

Me-to-Me | Moving funds between personal accounts across banks | Savings transfers, investment funding |

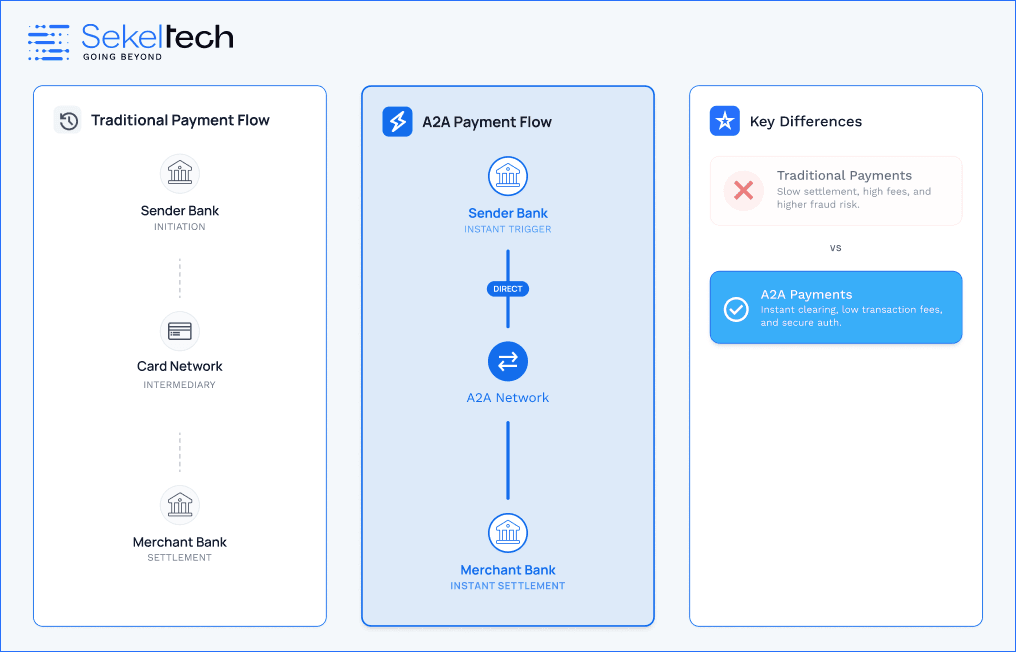

How Do A2A Payments Work?

The process is straightforward. The payer authorises a transfer, it moves through a payment rail, and the payee's account is credited. Here's what happens at each stage.

1. Initiation - The payer initiates payment through their banking app or a third-party provider. Push payments are started by the payer. Pull payments are initiated by the recipient with prior consent.

2. Authentication - The payer's identity is verified. Most regulated markets require two-factor authentication, a password plus fingerprint or one-time passcode.

3. Clearing and Settlement - The payment moves through the relevant rail. Real-time rails settle in seconds. Batch rails like ACH take one to three business days.

4. Confirmation - Both parties receive confirmation. The transaction is recorded and traceable.

A2A Payment Rails Explained

Payment rails are the infrastructure carrying money between accounts. Different markets use different rails.

Rail | Region | Speed |

UPI | India | Instant |

Faster Payments | UK | Instant |

PIX | Brazil | Instant |

SEPA Instant | Europe | Instant |

ACH | United States | 1-3 days |

BACS | UK | 3 days |

How Long Does an A2A Payment Take?

Depends on the rail. Real-time rails like UPI and Faster Payments settle in seconds, any time of day. Batch rails like ACH take one to three business days. The global trend is clear though. Instant settlement is becoming the default standard across most major markets.

What Are A2A Payments Used For?

Account-to-account payments have applications across industries and transaction types. Here are the most common use cases.

1. Retail and E-commerce

Customers pay for online purchases directly from their bank accounts without entering card details. Businesses issue refunds instantly back to the customer's account. No processing delays. No chargeback disputes.

2. B2B Supplier Payments

Businesses pay suppliers, contractors, and vendors directly between bank accounts. A2A payments simplify cash flow management and integrate with ERP systems to automate reconciliation. Large invoice payments move without card network fees eating into margins.

3. Payroll and Salary Transfers

Businesses pay employee salaries directly to bank accounts. Faster, cheaper, and more reliable than paper checks. Gig workers and freelancers receive payments from platforms or clients instantly without intermediary delays.

4. Subscription and Recurring Payments

Pull-based A2A payments handle subscriptions, utility bills, loan instalments, and insurance premiums automatically. The payer authorises once. Payments run on schedule without manual intervention.

5. Government and Public Sector

Tax payments, benefit disbursements, and social security transfers move directly between government and citizen bank accounts. Faster distribution, lower administrative cost, full traceability.

6. Cross-Border Payments

A2A infrastructure is increasingly used for international transfers. SEPA handles cross-border account-to-account payments across Europe. Emerging corridors in Asia and Latin America are building similar rails to reduce the cost and speed gap in global money movement.

7. Investment and Personal Finance

Investors fund accounts or withdraw portfolios directly. Individuals move money between personal accounts across banks. Charitable donations reach organisations without card processing fees reducing the contribution.

Benefits of A2A Payments

Businesses and consumers switching to account-to-account payments gain advantages that compound over time. Here are the most significant.

1. Zero or Low Transaction Fees

Card payments carry MDR charges, processing fees, and settlement costs. A2A payments bypass card networks entirely. No MDR. No wallet commissions. No hidden fees.

For businesses processing high transaction volumes, the savings are significant. A retailer paying 2% MDR on ₹10,000 daily transactions pays ₹200 every day just in fees. A2A eliminates that cost entirely.

2. Instant Settlement

Real-time A2A rails settle payments in seconds. Working capital isn't stuck waiting for a two-day card settlement window. Distributors receive payment instantly. Reorder cycles shorten. Cash flow improves across the entire supply chain.

3. Full Payment Traceability

Every account-to-account payment is digitally recorded and traceable. Businesses know exactly when payment was sent, received, and confirmed. Disputes reduce. Reconciliation becomes automated rather than manual.

4. Improved Working Capital

Faster settlement means money moves through the business faster. Suppliers get paid sooner. Distributors reorder sooner. The entire supply chain operates with less friction and less capital tied up waiting for payments to clear.

5. Enhanced Security

A2A payments use strong customer authentication and bank-grade security protocols. There are no card details to steal. No payment credentials exposed to third parties. Fraud risk is significantly lower compared to card-based transactions.

6. Cleaner Transaction Data

Every A2A payment generates structured, validated transaction data. Verified identities. Geo-tagged locations. Traceable payment histories. This data feeds directly into CRM systems, distribution analytics, and compliance reporting without manual cleaning or reconciliation.

A2A Payments vs Other Payment Methods

How do account to account payments compare to the alternatives? Here's a direct comparison.

A2A Payments | Credit Cards | Digital Wallets | Wire Transfers | |

| Transaction Fees | Zero or minimal | 1-3% MDR | 0.5-2% | Fixed fee per transfer |

| Settlement Speed | Instant to 1 day | 2-3 days | Instant to 1 day | 1-5 days |

| Fraud Risk | Low | Higher | Medium | Low |

| Chargeback Risk | None | High | Medium | None |

| Infrastructure Required | Bank account | Card terminal | App or wallet | Bank account |

| Cross-Border | Growing | Widely available | Limited | Widely available |

| Data Quality | High | Medium | Medium | High |

| Best For | B2B, recurring, distribution | Consumer retail | P2P, small purchases | Large one-off transfers |

Key Takeaways

Card payments are widely accepted but expensive. Every transaction carries MDR that erodes margins, especially for businesses operating on thin distribution margins.

Digital wallets are convenient for consumers but add a layer between the payer and payee. Fees and settlement delays still apply.

Wire transfers work for large one-off payments but are slow, expensive, and manual. Not practical for high-frequency distribution payments.

Account to account payments win on cost, speed, traceability, and data quality for businesses moving money regularly across supply chains, distribution networks, and recurring payment cycles.

Global Impact and Market Adoption of A2A Payments

A2A payments are no longer emerging. They're the dominant payment infrastructure in several major markets and growing fast everywhere else.

- A2A Payment Adoption in Europe

Europe leads global A2A adoption driven by open banking regulation. PSD2 mandated banks to open infrastructure to third-party payment providers, creating the foundation for widespread account-to-account growth. SEPA Instant now enables real-time A2A transfers across 36 countries. The Netherlands, Poland, and the Nordics have among the highest adoption rates globally.

- A2A Payment Adoption in Asia

Asia presents the most diverse A2A landscape globally. Japan, South Korea, and Singapore have mature instant payment infrastructure. Southeast Asia is rapidly building real-time A2A rails through PayNow in Singapore, PromptPay in Thailand, and DuitNow in Malaysia.

- A2A Payment Adoption in India

For anyone still unclear on A2A payment meaning, India's UPI is the clearest real-world example. Built and governed by the National Payments Corporation of India, it processes over 10 billion transactions monthly on pure A2A rails. Instant, zero MDR for most transactions, accessible to anyone with a bank account and mobile number. According to McKinsey's 2025 Global Payments Report, A2A payments now account for approximately 30% of global point-of-sale volume, led by markets like India, Brazil, and Nigeria.

- The Future of A2A Payments Globally

The direction is clear. Real-time, low-cost A2A infrastructure is becoming the global standard. The G20 has made faster cross-border payments a priority. ISO 20022 is being adopted across major payment rails worldwide. As open banking expands beyond Europe into Latin America, the Middle East, and Southeast Asia, A2A payments will increasingly replace card-based transactions for both consumer and business payments.

How Sekel Tech Powers A2A Payments for Retail Brands

The Problem With Fragmented Distribution Payments

Most brands still run distribution on fragmented payment logic.

C&F settles one way. Distributors collect another. Dealers reconcile manually. Retailers pay via mixed rails. Money moves but visibility doesn't. Disputes accumulate. Working capital gets stuck. Margins leak before the product reaches the end customer.

The problem isn't the payment volume. It's payment structure. And that's exactly where A2A payments change everything.

How Sekel Tech Embeds A2A in Closed-Loop Distribution

Sekel Tech embeds account-to-account payment infrastructure inside a closed-loop system. Every payment is mapped to a verified location, role, and transaction event.

Collections, incentives, and distributor settlements all move on A2A payment rails. No card MDR. No wallet commissions. No hidden settlement delays. Margins stay protected at every layer of the chain.

Clean CRM data from day one. Validated identities. Geo-tagged outlets. Traceable transactions. Digital onboarding brings the network in. A2A accelerates capital flow. Closed-loop execution ensures nothing leaks in between.

From C&F to Retailer: A2A Across the Full Chain

Here's what account-to-account payment embedded distribution looks like in practice:

Stage | What A2A Enables |

| C&F → Distributor | Instant settlement, traceable collections |

| Distributor → Dealer | Real-time payment confirmation, reorder triggers |

| Dealer → Retailer | Zero MDR transactions, digital reconciliation |

| Retailer → Customer | Instant A2A payment, service eligibility verified |

| Returns and Replacements | Automated refund processing, no manual disputes |

Every payment is tagged to a location. Every settlement was confirmed in real time. Reorder cycles shorten. Working capital improves across every tier.

Smart EPOS With A2A Integration

Even in B and C tier towns, a retailer onboards securely with just a mobile number. Government-validated business data is auto-fetched. The interface is intuitive and available in regional languages.

Because payments are A2A through Sekel Tech's Smart EPOS:

- No credit card MDR

- No wallet commissions

- No hidden settlement fees

- Zero cost burden on retailer or end customer

Small retailers transact digitally without card terminals. A2A payment meaning becomes tangible here. Every transaction is instant, traceable, and margin-protected from the first sale.

Watch how Sekel Tech helps brands manage listings, payments, and sales all from one place.

Warranty and Service Management Powered by A2A

Brand-driven service requests and warranty claims are handled in real time irrespective of where the product was purchased.

As long as the customer reaches an authorised dealer, Sekel Tech's system verifies the account-to-account payment transaction and processes service requests, warranty validation, and replacement workflows instantly, at the outlet or online.

No manual verification. No inter-dealer disputes. No customer frustration.

That's not just digitisation. That's a structured, scalable distribution built on A2A payment infrastructure.

Frequently Asked Questions (FAQ's)

1. What does A2A payment mean?

A2A payment stands for account-to-account payment. It means money moves directly from one bank account to another without card networks or payment processors in between. Faster, cheaper, and more traceable than traditional payment methods.

2. Is A2A the same as ACH?

Not exactly. ACH is one payment rail used for A2A payments in the United States. A2A is the broader concept. ACH, UPI, Faster Payments, PIX, and SEPA are all different rails that carry account to account payments in different markets.

3. Is A2A payment safe?

Yes. A2A payments authenticate directly with the payer's bank using strong customer authentication. No card details are shared or stored. Nothing sensitive is exposed to third parties. Fraud risk is significantly lower compared to card-based transactions.

4. Is UPI an A2A payment?

Yes. UPI is one of the most successful A2A payment schemes in the world. Built by the National Payments Corporation of India, it moves money directly between bank accounts instantly with zero MDR. India processes over 10 billion UPI transactions monthly.

5. Can A2A payments be automated?

Absolutely. Pull-based account to account payments automate recurring transactions like subscriptions, payroll, and supplier settlements. In distribution networks, A2A enables fully automated payment flows triggered by order confirmations, delivery events, and reorder cycles without manual intervention.

Conclusion

A2A payment is no longer a niche concept reserved for fintech insiders. Account-to-account payment infrastructure is actively reshaping how businesses move money across retail, distribution, e-commerce, payroll, and cross-border transactions globally. The A2A payment meaning goes beyond simple bank transfers. It represents a fundamental shift toward faster settlement, lower costs, better data, and cleaner distribution operations at every layer of the supply chain. For retail and distribution brands looking to eliminate payment friction, protect margins, and build scalable operations, embedding A2A payments into closed-loop distribution infrastructure is no longer optional. It's the direction the entire payments industry is moving. Sekel Tech makes that transition structured, measurable, and immediately operational for brands of every size. Explore Sekel Tech's A2A Payment Solutions.

Read More Blogs -

1. Geo Task Manager: Turn Daily Insights into Revenue Growth

2. Multi-Location Content Management Platform: Complete Guide

Share

Similar Blogs

Loved this content?

Sign up for our newsletter and get the latest tips & updates directly in your inbox.

There’s more where that came from!